How can a sole proprietor avoid double taxation of the unified social contribution?

How can a sole proprietor avoid double taxation of the unified social contribution?

The author of the article: Denis Korablyov

Many Ukrainian entrepreneurs combine their own business with hired work. This is convenient: there is a stable income from the company and additional opportunities as a sole proprietor. But at the same time, the question arises – will you have to pay the unified social tax twice: as an entrepreneur and as an employee? It is important to understand this situation in order to avoid unnecessary expenses, keep records correctly and not create problems with the tax authorities.

Contents of the article

Imagine: you are a sole proprietor, but you also work in an office as an employee. And suddenly the question arises – won’t you have to pay the unified social tax twice? Once as an entrepreneur, and once as an employee? Why is this important right now? More and more entrepreneurs combine their business with their full-time jobs. Some are hedging their bets, some receive a stable income, and some simply cannot refuse an interesting project. And here a real unified social tax puzzle arises.

Is it necessary to pay the unified social contribution twice if the individual entrepreneur works as an employee (on the staff of a legal entity)?

Good news right away: From January 1, 2021, you do not need to pay the unified social tax twice. This rule has significantly simplified the life of individual entrepreneurs who work in parallel on staff or cooperate under a gig contract.

Let’s take an example. Imagine Irina is a private entrepreneur in the third group, an IT specialist. Since the beginning of the year, she signed a gig contract with a resident of Dia City, and a little later she was invited to a startup for the position of team lead. For several months, Irina received both her private entrepreneur income and a salary from her new employer. In order to avoid unpleasant surprises with the tax office, Irina decided to pay the unified social contribution “for herself” as a private entrepreneur, and the company simultaneously paid the unified social contribution for her as an employee. Then it turned out that these contributions were not discouraged, and the state would not thank him for his “additional seniority”. As a result, she had to write a statement to the tax office to return the overpayment.

This rule also applies to persons who have entered into a gig contract with a resident of Diya City. Thus, individual entrepreneurs who have a main place of work or work under a gig contract may not pay the unified social tax “for themselves” if the contribution is paid in full by the employer or a resident of Diya City.

In simple terms: whether it’s a regular employer or a Day City resident, the principle is the same. Someone pays the minimum contribution for you, and that’s it – you’re free from double payments.

*Regulatory framework

Part 1 of Article 4 of Law No. 2464: payers of the Unified Social Contribution are individual entrepreneurs, including payers of the single tax (except for e-residents).

Part 6 of Article 4 of Law No. 2464: entrepreneurs who have a main place of work or who have entered into a gig contract with a resident of Deya City are exempt from paying the unified social tax for themselves for those months for which the employer (or resident of Deya City) has paid a contribution of at least the minimum.

What to do if the contribution is less than the minimum or when should a sole proprietor pay the unified social tax independently?

Let’s assume that your employer or a resident of Deya City paid the unified social tax for you in an amount less than the minimum established, while the entrepreneur must independently calculate and pay the difference.

For example, the employer paid 1000 UAH for you, and the minimum contribution is 1902,34 UAH. This means that as a sole proprietor you must pay an additional 902,34 UAH. Not very pleasant, but better than paying the full amount twice.

Please remember that the amount of the unified social contribution cannot be less than the minimum contribution (22% of the minimum wage) and cannot be more than the maximum amount.

Voluntary payment of the unified social tax: is it allowed?

According to the IPC of the State Tax Service dated 01.11.2021 No. 4139/IPK/99-00-04-03-03-06, if the employer paid the sole proprietor the unified social contribution in an amount not lower than the minimum, the sole proprietor does not have the right to voluntarily pay the unified social contribution for himself. So, if you suddenly decided to pay “for safety” – this is a violation. You have this right only in those months when the employer paid less than the minimum contribution.

What to do with overpayment?

If the individual entrepreneur has nevertheless paid the unified social contribution “for himself” for the months for which the employer has already paid:

such amounts are considered to have been paid in error or overpaid;

they can be applied towards future payments;

or return upon application submitted in the form specified in Appendix 1 of Procedure No. 6.

It is important to remember that, unfortunately, a sole proprietor will not receive double insurance experience, and this will not affect sick leave, maternity leave or pension. The state does not reward “excessive zeal”.

Do you want to consult with a specialist as quickly as possible?

Leave a request and our specialist will contact you shortly

Do you need to report anything additional to the tax office? No! All information comes from your employer automatically.

Individual entrepreneurs on the simplified taxation system (groups 1–3), exempt from paying the unified social contribution “for themselves”, do not complete or submit Appendix 1 to the tax return if the conditions of parts 4 and 6 of Article 4 of Law No. 2464 are met.

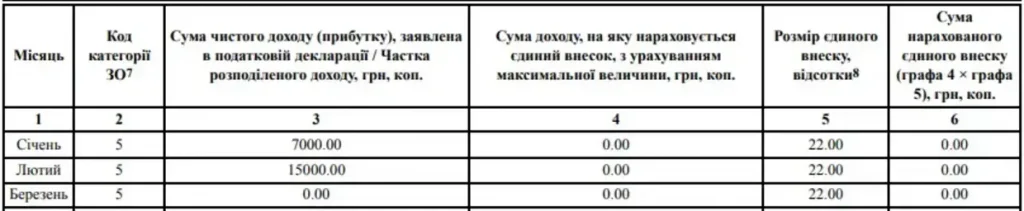

For months when the Unified Social Contribution was paid for you by your employer, you must complete the Unified Social Contribution Appendix as follows:

*There is no need to additionally inform the tax office that the single social contribution is paid by the employer (since the tax office sees this in the employer’s reporting).

The Appendix to the declaration must be reflected as follows:

Appendix 1

in the Declaration of the single tax payer

Appendix 2

in the Declaration of Property Status and Income

*IPC dated 15.01.2025 No. 173/IPC/99-00-24-03-03 IPC focused on the aspects of payment of the unified social contribution by individual entrepreneurs who have a primary place of work. They once again emphasized that an individual entrepreneur who has a primary place of work is exempt from paying a single contribution for himself for the months of the reporting period for which the employer paid an insurance contribution for such person in an amount not less than the minimum insurance contribution (in 2025).

In this case, Appendix 1 to the Declaration is not filled in and is not submitted. Such persons may submit Appendix 1 only if they voluntarily participate in the system of compulsory state social insurance.

*This applies to all individual entrepreneurs, regardless of the chosen tax system.

How to get back an erroneously paid unified social tax?

If it so happens that you have overpaid or mistakenly paid the unified social contribution, you can return it. To do this, you should submit to the tax service to which the funds were credited, an “Application for the return of funds from accounts 3556” (the form is provided in Appendix 1 to the Procedure for crediting and returning the unified social contribution). The same application is submitted for the return of the unified social contribution paid for employees.

You can submit an application through the taxpayer’s electronic account (section “Correspondence with the State Tax Service”).

The IRS will not refund you if you have a tax debt. And by the way, if you decide not to refund the overpayment, it can be applied to future payments.

It should be noted that the tax office often refuses to return overpaid single social contribution without conducting a tax audit of the individual entrepreneur. Therefore, be prepared for the fact that the process may be delayed. Such funds can be returned within 1095 days (3 years) from the date of payment (from the date of their payment).

Useful video

Individual entrepreneur in Ukraine + individual entrepreneur abroad – how to avoid double taxation and fines?

Frequently asked questions

1) Did the employer pay the unified social contribution in an amount less than the minimum or did not pay the unified social contribution at all?

In the month of hiring or dismissal, as well as in certain other cases, the employer may pay the unified social contribution for you in an amount less than the minimum. In such a situation, the individual entrepreneur must independently pay the unified social contribution for himself for these months. There are also situations when the employer completely “forgets” about the unified social contribution. What to do? Do not panic, but do not ignore it either – you will have to pay the extra yourself.

*If the employer or Action City resident has paid the unified social contribution for you in an amount less than the minimum established, the entrepreneur is obliged to independently calculate and pay the difference. In this case, the amount of the unified social contribution cannot be less than the minimum contribution (22% of the minimum salary) and not more than the maximum amount.

2) Can a sole proprietor pay the unified social tax for himself if his employer has already paid it?

No. If the employer has paid the unified social tax in an amount not less than the minimum, you do not have the right to pay extra for yourself. What happens if you pay anyway? These funds will be automatically counted as an overpayment. The result: extra costs without benefit. Example: the employer paid 1902,34 UAH for you, and you additionally transferred another 1902,34 UAH as a sole proprietor. The result: you have an overpayment of 1902,34 UAH, which must be returned or credited for the future.

3) Is it necessary to notify the tax office if a sole proprietor simultaneously works as an employee?

No. You do not need to inform the tax office separately that you are an employee. The law does not provide for such an obligation. It’s simple: the tax office receives all the necessary information from your employer’s reports. They see how much and for whom the single social contribution was paid, so your additional reports will be superfluous.

To prevent the Unified Social Contribution from becoming a headache – your mini-guide

The most annoying mistake is when you pay more than you need to, or to the wrong place. And all because of a trifle that could have been clarified in 5 minutes. So let’s fix it:

Do not rush to pay the unified social tax “for yourself” if you have a main place of work or a gig contract – first check whether everything has already been paid by the employer!

Be sure to check that the contribution is not less than the minimum. If you are short, pay the difference and you can sleep soundly.

If you overpaid, don’t put off the issue of getting your money back.

Don’t be shy about asking for advice: it’s better to ask an accountant one question now than to deal with overpayments or fines later. Attention to detail in taxes is always a profitable investment.

Would you like to discuss this issue in particular?

Leave your request and our facists will call you as soon as possible